Maybe a friend brought it up. Maybe it came up when you finally sat down to redo your will, or after a relative passed and the family spent the better part of a year tangled in court. However you landed here, one question is on your mind: what is a family trust, and is it something your family really needs?

Here is the short answer. A family trust is a legal arrangement that holds your assets for the people you care about, whether that is a spouse, your kids, or your grandkids. You decide who gets what. You decide when they get it, and on what terms. Done right, the whole thing can sidestep probate, the slow and very public court process that sorts out estates in New York.

This guide keeps things plain. We will walk through what a family trust really means, how one works under New York law, who ends up owning the assets, and whether setting one up is worth it for you. No legal fog.

Family Trust, Defined

Strip out the legal language and a family trust is pretty simple. One person puts assets into the trust. Those assets get managed for the benefit of family members. That is the core of it.

The assets can be almost anything you own. A house. A co-op in Queens. Bank accounts, investments, a stake in the family business. Once you create the trust and move property into it, that property is held by the trust and handled by the rules you wrote down.

A lot of people look up the family trust meaning and brace for something dense. It is not. Picture a box with a set of instructions taped to the lid. You fill the box with property, you spell out how it should be used and who it goes to, and you hand the keys to someone you trust. New York law makes those instructions binding, so they hold up even after you are gone.

A family trust is only one tool among several. To see how it stacks up against the alternatives, our guide to the different types of trusts breaks each one down.

- Family Trust, Defined

- How a Family Trust Works in New York

- Who Owns the Assets in a Family Trust?

- Revocable or Irrevocable: Which Family Trust Fits?

- Revocable or Irrevocable: Which Family Trust Fits?

- How to Set Up a Family Trust in New York

- Family Trust FAQs for New York Families

- Talk to a New York Trusts Attorney

How a Family Trust Works in New York

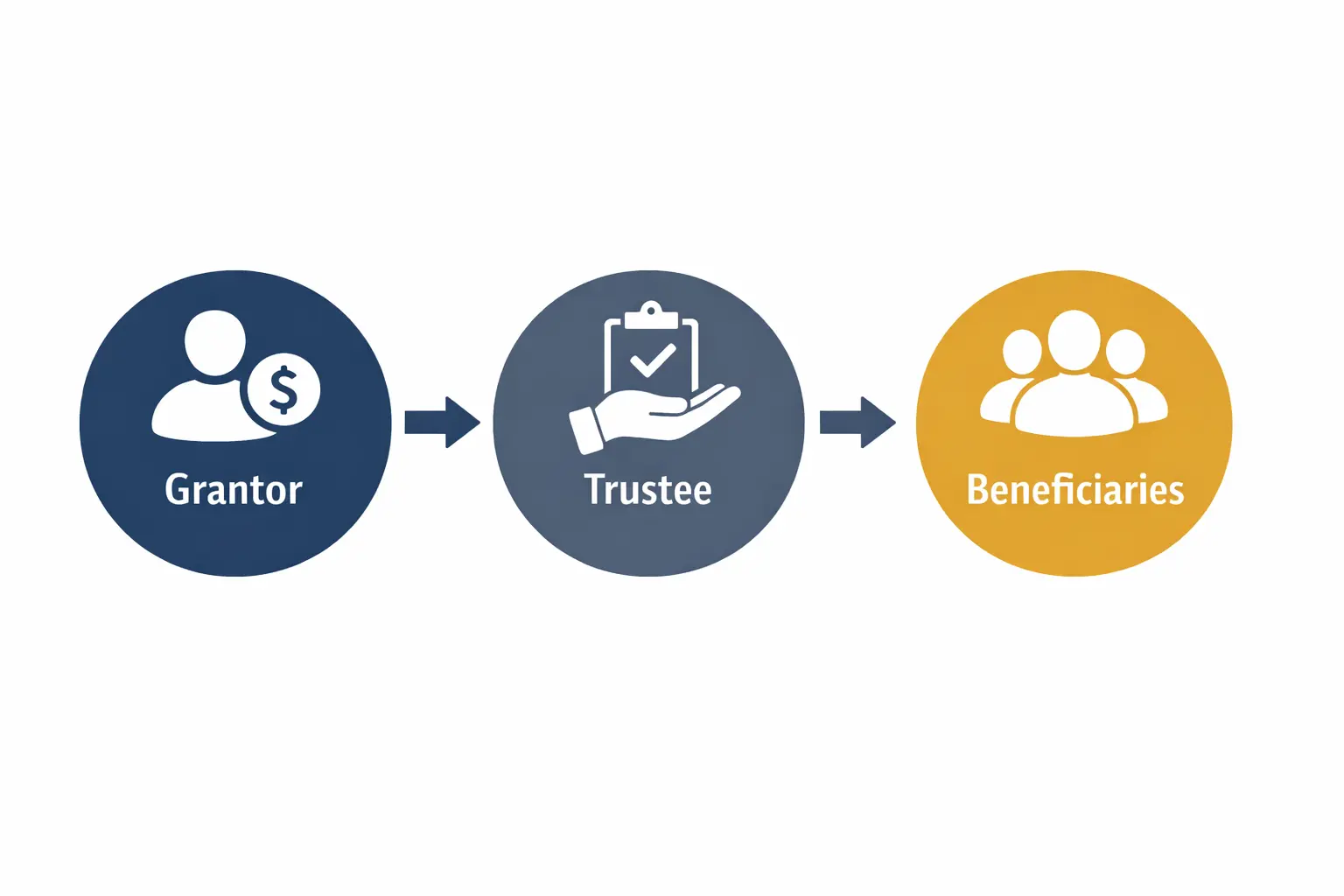

Every trust runs on three roles. Once you see who they are, the whole thing clicks into place.

The Grantor

That is you, assuming you are the one setting it up. The grantor creates the trust and decides what goes inside. You might also hear the words settlor or trustmaker tossed around. Same job, different label. You pick the assets, the beneficiaries, and the rules.

The Trustee

The trustee runs the trust. This is the person or institution that holds legal title to the assets and has to manage them honestly, in the interest of the beneficiaries. New York takes that obligation seriously and gives it a name: fiduciary duty. Plenty of people serve as their own trustee while they are alive, then name a successor to take the reins later. Others hand the job to a relative they trust, a close friend, or a professional such as a bank or an attorney.

The Beneficiaries

These are the people who benefit. A beneficiary might collect income from the trust, get the right to live in a home, or receive a share of the assets at a set point in time. You can give different beneficiaries different rights, and that flexibility is a big part of why families lean on trusts. One common setup supports a surviving spouse for life, then passes whatever is left to the children.

String the three together and you have the whole machine. You hand assets to a trustee. The trustee manages them for your beneficiaries. The rules you wrote control everything else.

Picture it with a real family. A couple in Brooklyn owns a brownstone that has roughly tripled in value since they bought it. They have two kids, both under ten. They set up a family trust, name themselves as trustees, and list the children as beneficiaries. Day to day, nothing changes.

They live in the house, pay the bills, carry on as normal. But if both parents die, the successor trustee they chose steps in, takes over the home and the savings, and releases money for the kids’ schooling and care. No year lost in Surrogate’s Court. No file open for the public to read.

Who Owns the Assets in a Family Trust?

This one trips people up. Once you move an asset into a family trust, the trust owns it. Not you, at least not on paper. The trustee holds and manages it, but only for the beneficiaries, never for personal gain.

What that means for you comes down to the kind of trust. With a revocable family trust, you usually stay firmly in the driver’s seat while you are alive. Move assets in, pull them back out, rewrite the terms, scrap the whole thing if you change your mind. For tax purposes, the law still counts the property as yours.

An irrevocable family trust is a different animal. Once assets go in, they generally stay in, and you hand over a good deal of control. That sounds like a downside, and sometimes it is. But it is also the trade that unlocks the bigger benefits, like real protection from creditors and possible estate tax savings.

So why does ownership matter this much? Because it drives nearly everything else: your taxes, whether a creditor can reach the assets, even eligibility for certain benefits. It is also the line that separates the two main types of family trust, which is exactly where we head next.

Revocable or Irrevocable: Which Family Trust Fits?

Nearly every family trust lands in one of two camps, and the choice colors everything that follows.

A revocable family trust bends to your will. Change it, add to it, or tear it up entirely, any time you are alive and of sound mind. It is flexible, easy to live with, and it does a fine job of avoiding probate. The catch is protection, or the lack of it. Since the law still treats the assets as yours, a revocable trust shields you from neither estate tax nor creditors.

An irrevocable family trust barely budges once it is signed. In return for that stiffness, it can lift assets out of your taxable estate, put them beyond the reach of many creditors, and support long term care planning. For wealthier New York families, those advantages can be worth a great deal.

Here is the New York wrinkle. The state runs its own estate tax on top of the federal one. For deaths in 2026, the New York exclusion sits at $7.35 million, and the state enforces a quirky rule people call the estate tax cliff. Climb past roughly 105 percent of that figure and you can lose the exclusion altogether, owing tax on the entire estate from the first dollar up. The official numbers live on the New York State Department of Taxation and Finance site. For a fuller breakdown, see our NY Estate Tax Guide.

Picking between the two is not a coin flip. Our guide on revocable or irrevocable trusts sets them side by side so you can weigh the trade offs honestly.

Revocable or Irrevocable: Which Family Trust Fits?

No tool fits every family, and a family trust is no exception. Here is the straight version of both sides.

The Benefits

The Drawbacks

How to Set Up a Family Trust in New York

The path is fairly clear. Pick the right type of trust. Decide which assets belong in it. Name your trustee and your beneficiaries. Have an attorney draft the document, then sign it the way New York requires. Last, fund it by retitling your assets into the trust’s name. That final step is the one people skip, and it is the one that makes everything else real. Funding can also brush up against federal gift rules, so the IRS gift tax guidance is a sensible place to start.

We lay out every step in our guide on how to set up a trust in New York.

Family Trust FAQs for New York Families

Talk to a New York Trusts Attorney

A family trust is one of the strongest ways to look after the people who matter most. But the details are where it lives or dies. New York’s estate tax cliff, its probate rules, the gap between a revocable and an irrevocable trust: each one leaves room for an expensive mistake when the document is drafted without real care.

That is the part we handle. At Bartal Law, we build trusts for New York families that fit their lives and actually hold up when the day comes. Whether you are starting fresh or dusting off a plan from a decade ago, we will talk you through every option in language that makes sense.