Here is a scene I have lived through more times than I can count. Someone walks in holding a thick binder. A beautiful trust, drawn up years ago, signed and notarized and tucked away. They feel good about it. Then I ask one simple question. Did you ever move anything into it? Silence. The house is still in their own name. So is the brokerage account. The trust, gorgeous as it looks, owns nothing.

That empty trust problem is the most common mistake I see. The fix is not hard. It just gets skipped.

So let us talk about the part nobody finishes. Funding. Which assets belong in your trust, which ones should stay far away from it, and how you actually retitle the whole lot here in New York. If you have not built the trust yet, start with our step by step guide on how to set up a trust in New York, then come back here for the funding piece.

What funding a trust actually means

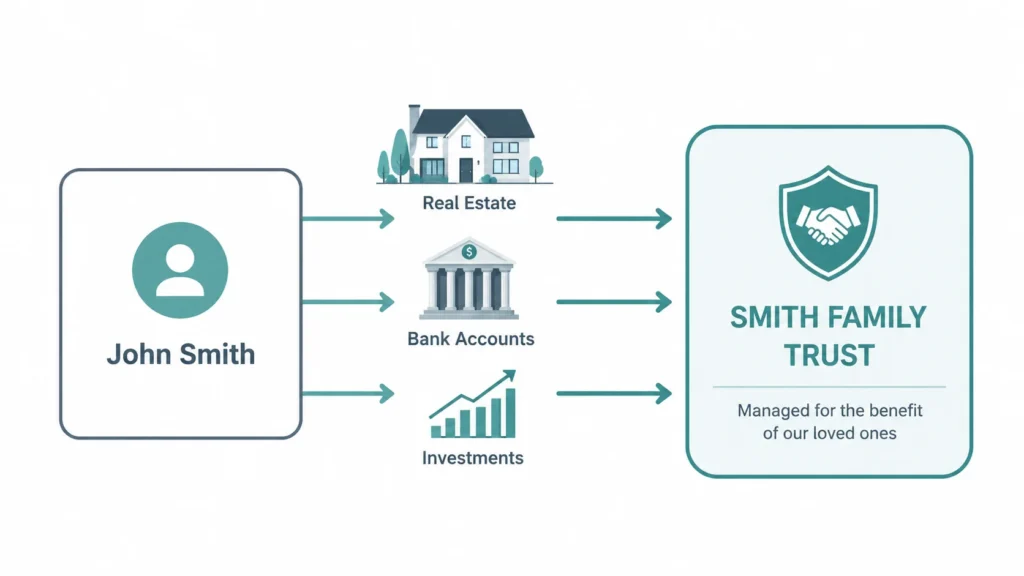

Funding is just a fancy word for moving assets into the name of your trust. That is it. You take something you own personally, your home, say, and change the legal owner so the trust holds it instead of you.

Think of the trust as an empty basket. Signing builds the basket. Funding fills it. An unfilled basket feeds no one.

Why does this matter so much? Because a revocable living trust earns its keep by keeping your estate out of probate, the court supervised process that runs through New York’s Surrogate’s Court. But here is the catch most people miss. Probate only skips the assets the trust actually owns. Anything still in your own name when you pass goes through the court anyway, trust or no trust. So an unfunded trust does not save your family one single trip to Surrogate’s Court.

I had a client out in Massapequa, a retired teacher, who set up a trust with a different firm and never funded it. When she passed, her kids spent the better part of a year in probate over a house the trust was supposed to protect. Avoidable. For more on how this structure works, see our piece on setting up a living trust in New York.

Assets you should put in a trust

Not everything you own needs to go into the trust, and we will get to the exceptions in a minute. But a good chunk of what most New York families hold belongs inside it. Here is where I usually start when I sit down with someone.

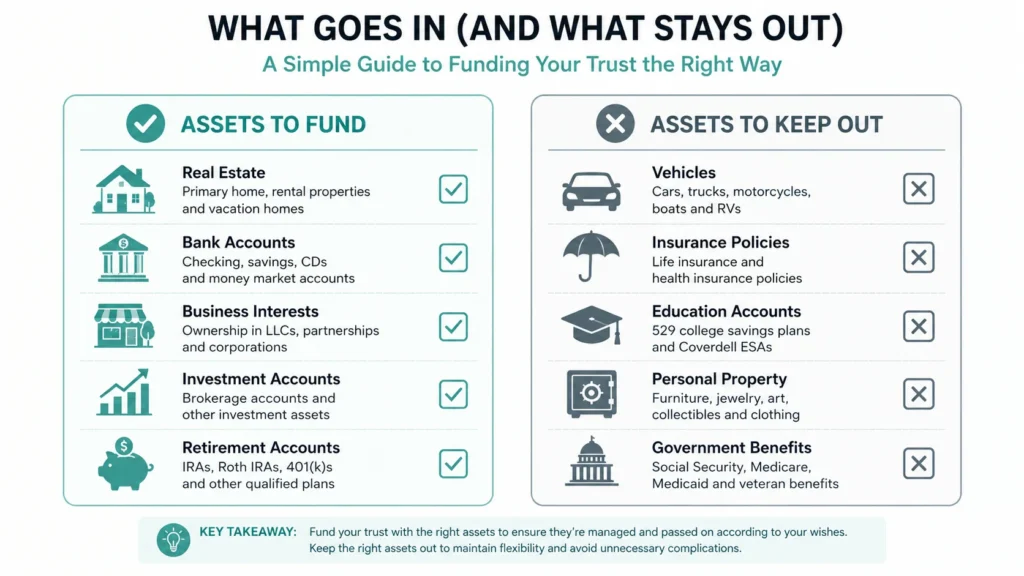

Real estate

Your home is almost always the big one. For most families it is the largest asset they own, and it is exactly the kind of thing that drags an estate into probate when it sits in an individual name. Retitle the deed so the trust is the owner, and the property passes straight to your beneficiaries without the courthouse.

This goes for more than your primary residence. That cabin upstate. The two family in Bay Ridge you rent out. A condo down in Florida. Out of state property is a big one, because real estate normally gets probated in the state where it sits, which can mean a second probate in a second state. A trust sidesteps that headache.

One New York wrinkle worth flagging. If your home carries a STAR exemption or you are counting on certain property tax breaks, the way the trust is drafted matters. Done right, you keep those benefits. Done sloppily, you can lose them. This is one of those spots where a template off the internet quietly costs you. Our Wills and Trusts services handle the deed work so nothing slips.

Bank accounts and CDs

Checking, savings, money market accounts, certificates of deposit. These can all be retitled into the trust, and for larger balances it usually makes sense. You walk into the bank, show them the trust, and they reissue the account in the trust’s name. You still use the money as before.

Now, a small caveat. You probably do not want your everyday checking account, the one that pays the electric bill, tangled up in the trust if it complicates your daily life. Some folks keep a modest operating account in their own name with a payable on death beneficiary and move the bigger balances into the trust. There is no single right answer here. It depends on how you live.

Investment and brokerage accounts

Non retirement investment accounts are prime candidates. Stocks, bonds, mutual funds, that taxable brokerage account that has quietly grown over twenty years. Retitling these keeps them out of probate and lets your successor trustee step in without missing a beat if you become ill or pass away.

Business interests

Own a piece of a business? Your shares in a closely held company, your membership interest in an LLC, your stake in a family partnership can often go into the trust too. This matters for continuity. If you run the corner bakery in Astoria and something happens to you, a funded trust lets your trustee step in and keep the lights on instead of the whole thing freezing in court.

That said, business interests come with strings. Operating agreements, buy sell provisions, sometimes partner consent. Do not assume you can drop your LLC into the trust over a weekend. Check the paperwork first, or have someone check it for you.

People also fund trusts with valuable personal property like art or jewelry, life insurance in certain setups, and intellectual property. The thread is the same throughout. If an asset would otherwise land in probate, and it can be retitled, it usually belongs in the trust. For how your beneficiaries eventually receive it, read how trust beneficiaries receive their inheritance.

Assets you should usually keep out

Just as important as what goes in is what stays out. Pour the wrong things in and you can trigger taxes, blow up benefits, or create a mess that costs more to unwind than it ever saved. A few categories deserve real caution.

Cars, for one. In most cases it is more trouble than it is worth to retitle a vehicle into a trust, and New York has simpler tools for transferring one at death. Health savings accounts are another. And active everyday checking accounts often do better left out with a beneficiary designation instead.

But the big one, the category that trips up almost everybody, is retirement accounts. That gets its own section, because the stakes are real.

Retirement accounts, the important exception

Please hear me on this one. Do not retitle your IRA or your 401(k) into your living trust during your lifetime. I mean it.

Here is why. Retirement accounts are tax deferred, and they are legally tied to you as an individual. The moment you transfer ownership of a traditional IRA out of your name, the IRS can treat the whole thing as a distribution. The entire balance could become taxable income in a single year. A lifetime of savings, taxed all at once. The mistake is almost always irreversible. The IRS rules on retirement account beneficiaries spell out how these accounts are meant to pass.

So how do you keep a retirement account out of probate without wrecking it? Beneficiary designations. You name your spouse, your kids, or in some cases a specially drafted trust directly on the account. The money skips probate and lands with the people you chose, no retitling required.

Naming a trust as the beneficiary of a retirement account can make sense, especially when you want to control how a young or vulnerable beneficiary receives the funds. But it has to be a particular kind of trust, drafted with the tax rules in mind. This is not a do it yourself moment. Get it wrong and you can shorten the payout window and inflate the tax hit.

How to retitle your assets in New York

Alright. You know what goes in and what stays out. Now the mechanics, because this is where momentum tends to die. The good news is each asset has its own clear path.

For real estate, you prepare and record a new deed that transfers the property from you to the trust. In New York that deed gets filed with the county clerk where the property sits, with recording forms and sometimes transfer tax considerations to handle correctly. This is the one I really do not recommend freelancing.

For bank accounts and CDs, bring the trust documents to the bank and they retitle the account in the trust’s name. For brokerage accounts, contact the custodian and complete their trust transfer paperwork. For business interests, you assign your shares or membership interest to the trust, after confirming the operating agreement allows it. And for anything passing by beneficiary designation, you simply update the form with the provider.

If you plan to fund the trust partly through gifts while you are alive, the federal gift tax rules come into play. For 2026 you can give up to $19,000 to any one person without filing a gift tax return, and the lifetime gift and estate tax exemption sits at $15 million. The IRS gift tax page covers the details, and these figures shift over time, so treat them as a 2026 snapshot.

A quick word on New York estate tax

One thing I always clear up, because people mix it up constantly. New York has an estate tax, not an inheritance tax. Your kids are not taxed simply for inheriting from you. The estate itself may owe tax before anything is distributed.

For 2026 the New York estate tax basic exclusion amount is $7,350,000. Stay under it and the state estate tax generally does not apply. Go over it and New York has a brutal cliff. Exceed the exclusion by more than five percent and you lose the exemption entirely, so the tax hits your whole estate from the first dollar. Funding a plain revocable trust does not lower this, because you still control the assets. Certain irrevocable trusts can. The state lays out the current numbers on its estate tax page.

Frequently Asked Questions

The bottom line

A trust is only as good as what you put in it. Build the basket, then fill it. Move your home, your non retirement accounts, and your business interests in. Keep your IRA and 401(k) out, handled with beneficiary designations instead. Retitle everything the New York way, so it holds when your family needs it.

That last mile, the funding, is exactly where we help New York families most. Whether you are in Queens, Brooklyn, the Bronx, Manhattan, or out on Long Island, we make sure the trust you paid for actually does its job. Take a look at how we work over at bartallaw.com, or reach out through our contact page and we will get your assets where they belong.