An emerging strategy for business owners and many individuals is placing Limited Liability Companies (LLCs) in trusts. Placing an LLC in a trust can provide a number of valuable legal and financial benefits, such as increased asset protection, more efficient estate planning, and the possibility for tax benefits. This guide is designed to provide information on the various components of LLC in trust structures, how to transfer ownership, and the benefits to consider in utilizing this strategy for managing wealth.

What Is a Trust and How Is It Related to an LLC?

Trusts are legal arrangements, and can be set up in a number of different ways. In the most common arrangements, the trustee of the trust holds legal title to the assets and manages these assets for the benefit of another. In the context of estate planning, trusts provide more versatile options for asset protection and wealth transfer. An LLC, or Limited Liability Company, is a business entity that provides the owners with the liability protection of a corporation, while also providing the owners the tax benefits and operational flexibility of a partnership. When these two entities are used together, the best aspects of both are used to create an LLC trust structure.

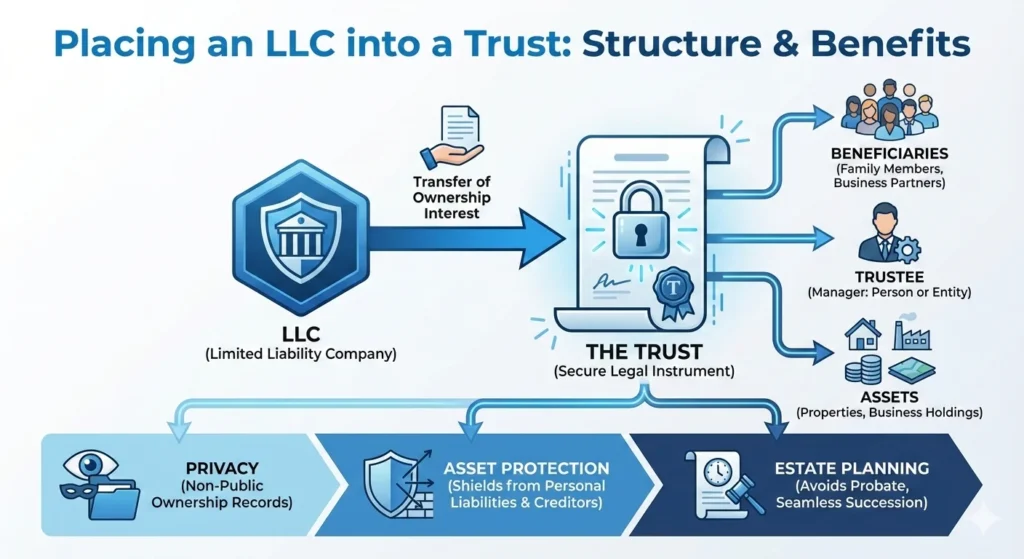

By setting up LLCs through trusts, business owners narrow down the risks of creditors going after their LLCs and, at the same time, are able to keep their business operational. Further, the LLC and trust combined mechanism offers ease of succession and estate planning, especially for business owners with substantial assets and legacies to protect.

Can an LLC Also Be Held in a Trust?

The answer is yes, and this is an estate planning and asset protection ‘best practice.’ Upon placing an LLC in a trust, the trust becomes the legal owner of the LLC membership interests while a trustee manages those interests for the trust beneficiaries.

The creation of a trust-owned LLC follows a straightforward process. It requires the existing LLC member to transfer their membership interest to the trust, subject to the operating agreement of the LLC and relevant state law for LLCs and trusts. Notably, the member’s interests become a part of the trust and pass to the trust beneficiaries at the member’s death, thus, circumventing probate.

Some common scenarios where placing an LLC in a trust is advisable may include:

- Estate planning where the aim is to avoid probate and ensure business continuation

- Protection of assets for high-net-worth clients

- Rental property management and/or management of a portfolio of real estate investments

- Succession planning in family businesses

Transferring ownership of an LLC to a trust has specific legal and procedural details that must be considered. Here is a step-by-step explanation of how to place an LLC in a trust:

Step 1: Establish or Identify Your Trust

The first step is to establish a revocable living trust (or if one already exists, then that trust) to be a holder of the LLC interest. The trust document must contain provisions for the management and distribution of the LLC interest.

Step 2: Examine the LLC Operating Agreement

If there are any provisions in the operating agreement that relate to the restriction of interests, understand that some agreements may require the approval of all members before the interest may be transferred. Moreover, you may be required to amend the operating agreement to provide that the new owner is the trust.

Step 3: Creation of a Membership Interest Assignment

The next step will be creating a Membership Interest Assignment that will transfer your LLC ownership to the trust. This document should specify the ownership percentage being transferred, the date of transfer, and the current owner’s and trustee’s signatures.

Step 4: Altering LLC Documents

You will need to change the LLC membership records to indicate the trust as the new owner and amend the issued membership certificates, if applicable.

Step 5: State Specific Documents

Depending on your state, ownership changes may require amendments to be filed with the Secretary of State. Be sure to review the state-specific guidelines for placing an LLC in a trust.

Step 6: New EIN

Generally, an LLC transfer to a revocable living trust should not require a new Employer Identification Number (EIN) since the trust is a disregarded entity. On the other hand, an irrevocable trust may necessitate a new EIN.

Important Reminder: This guide is meant to be a starting point for understanding the process involved in transferring an LLC’s ownership interest to a trust. It is important that you consult an estate planning attorney to comply with all legal requirements to enhance the value of this arrangement.

Can an LLC be a Beneficiary or a Trustee of a Trust?

The interplay between LLCs and trusts is multifaceted. Trusts may hold LLCs, and under specific conditions, LLCs may function as beneficiaries or as trustees.

LLC as Trust Beneficiary

Is it legally permissible for an LLC to be a beneficiary of a trust? Yes. Structuring a trust where an LLC is a beneficiary means that the LLC will be able to receive the trust’s assets and will be able to manage those assets subject to the LLC’s operating agreement. This is particularly advantageous when:

- The trust has managing income-producing assets that would benefit from the management of them by an LLC

- The trust has several family members who have an interest in the LLC and would like to simplify how distributions are made

- The business requires operational flexibility with how the assets are used

When an LLC is a beneficiary of a trust, the assets flowing from the trust to the LLC are managed according to the governing documents of the LLC. The members of the LLC receive distributions based on their ownership percentages.

LLC as a Trustee

Can an LLC act as a trustee? It depends. In most states, LLCs can serve as trustees, but some important considerations apply:

- There are complex estate planning situations where state laws may vary in allowing LLCs to act as trustees.

- The trustee LLC should have the authority, as well as the competence, to carry out fiduciary responsibilities.

- Some banks and other financial institutions may have reservations about dealing with an LLC as a trustee.

Using an LLC as a trustee may serve to maintain consistency in the management of a trust because, regardless of changes in members, the LLC will continue to operate. However, this necessitates a thorough design to ensure all state trust laws and fiduciary obligations are met.

Real Estate and the LLC Trust Model

An important consideration for real estate investors is how the LLC trust real estate model optimizes asset protection and estate planning. The following benefits are noteworthy for real estate owners: An LLC is created and is a member of the LLC (i.e., the owner of the LLC is a trust). The property is then held in the name of the LLC. The membership interests in the LLC are held by the trust. This structure provides multiple layers of protection: The LLC is a separate legal entity and provides protection from liability such that the personal assets of the owners are not at risk from lawsuits related to the property. The trust provides a means to avoid probate and is a vehicle for succession planning. The trust owner’s name is not in the public records, so increased privacy is afforded. The LLC member’s interest is subject to a charging order, so they have less protection from creditors.

Illustration: a real estate investor’s portfolio

Now consider a real estate investor who has several rental properties. Let us assume that she has formed an LLC for each property so she can serve liability isolation purposes. Each of these LLCs is owned by her revocable living trust. In the situation where a tenant sues over one property, only the assets of that property’s LLC are at risk.

She has no other properties that are at risk, nor are her personal assets. At her death, her heirs are granted ownership of the LLCs within the trust and they do not have to go through probate. This guarantees her heirs continuity of property management and rental income.

LLC vs Living Trust: Which Is Better for You?

For effective estate planning and asset protection, understanding the LLC vs living trust difference is critical. While they both protect individuals in legal situations and serve multiple purposes, they each operate differently and excel in different areas:

Limited Liability Company (LLC):

- Main function: Liability protection and operational function

- Tax treatment: Pass-through taxation (owners report LLC profits and losses)

- Protecting assets: Provides a shield for personal assets from business-related liabilities

- Avoiding probate: LLCs alone do not aid in avoiding probate.

Living Trust:

- Main function: Estate planning and aiding in avoiding probate.

- Tax treatment: In most situations, there is no need for a separate tax return (revocable trusts are treated as disregarded entities)

- Protecting assets: Offers minimal protection against the claims of creditors.

- Avoiding probate: This is a primary advantage — those who have a revocable trust will notice that the assets of the trust are not required to be probated, instead will pass to the beneficiaries.

The Advantage of Both:

Instead of deciding whether to have an LLC or living trust, many business owners find that an LLC in a trust offers the most advantageous combination. In this case, the LLC provides solid liability protection and operational simplicity, and the trust offers privacy and a simple mechanism for estate planning. This combination is ideal for business owners with a fair amount of assets and is especially helpful for owners of businesses who need to have both solid asset protection and effective succession planning.

Should I Put My LLC in a Trust?

The answer to the question “Should I put my LLC in a trust?” is not straightforward. Whether you put an LLC in a trust involves certain considerations such as your individual situation, financial objectives, and estate planning requirements. Here are some considerations:

Pros of Putting an LLC in a Trust:

- Avoid probate: Your interests in an LLC will delegate to the beneficiaries without a court order.

- Trusts are private. Trust ownership keeps your name out of the public record.

- If you are incapacitated, your successor trustee will step in and run the LLC.

- Your business will have a clear set of instructions for how it will operate after your death.

- Depending on your state and what type of trust it is, you may have tax savings.

Cons:

- It may cost you more to set up the trust and transfer ownership.

- You will have more paperwork, record-keeping, and administrative processes to manage.

- Some banks will not provide financing to LLCs owned by trusts.

- You may need to get the permission of the other members of the LLC to operate the trust.

When it makes sense:

Can you put an LLC in a trust? Yes, and you should put an LLC in a trust especially if you:

- Own a business or investment property that you want to pass to your heirs in a straightforward manner.

- Have considerable assets that need both estate planning and liability protection.

- Prefer to keep your business ownership confidential.

- Require a concrete succession strategy for your business.

- Have worries related to planning for potential incapacity and the continuity of your business.

Conclusion

An LLC combined with a trust is an excellent strategy for both protection of assets and estate planning. This is particularly true for people who are working with an LLC trust real estate arrangement for rental properties, or for people who are engaging in business succession planning. It is important to know how to transfer title of an LLC to a trust. The combined trust and LLC structure provides greater privacy, avoidance of probate, and simplified management, all of which are more important as your assets increase.

This guide has a lot of information regarding an LLC in a trust, and while we have done our best to provide as much as possible, every circumstance is different. Before you decide to pursue the option of putting your LLC in a trust, you should speak to an estate planning attorney and a tax advisor who specialize in your specific situation, as they will help you understand the best strategies to avoid traps and maximize your situation.