Setting money aside for your child is one thing. Making sure that money reaches them at the right age, for the right reasons, and without a court deciding how it gets spent is something else entirely. That is where a trust comes in. If you have been searching for how to set up a trust fund for a child in New York, you already sense that an ordinary savings account will not give your family the control or the protection you actually want. A trust will. It lets you decide who manages the money, when your child can touch it, and what it may be used for, long after you are gone.

This guide walks a New York parent through everything that matters. You will learn what a child’s trust really is, the trust types you can choose from, the exact steps to create one, what it tends to cost, and the quiet mistakes that undo good intentions.

What a Child’s Trust Fund Actually Is

A trust fund is not a special account you buy from a bank. It is a legal arrangement. You, the person creating it, hand assets to someone you choose, the trustee, who holds and manages those assets for the benefit of your child, the beneficiary. The rules that govern every dollar are the ones you write into the trust document. You set the ages, the conditions, and the limits, and the trustee is legally bound to follow them.

That single feature is what separates a trust from almost every other option a parent has.

So how does a trust fund work for a child in practice? You set the terms once, then the trustee carries them out for years. Money can grow inside the trust, distributions can be tied to age or to needs like education and housing, and your child never has to manage a large sum before they are ready. The instructions you write today keep guiding the money long after the conversation is over.

A trust fund versus a regular bank account

If you open a savings account in your child’s name, the money becomes theirs the moment they reach adulthood. There are no strings, no guidance, and no protection from a poor decision made at 18. A trust keeps the money in skilled hands and releases it on a schedule you design, whether that is at 25, in stages across their twenties, or only for specific needs like tuition or a first home.

A trust fund versus a UTMA custodial account

Many parents begin with a UTMA custodial account because it is simple to open and useful for modest sums. The catch is that the money turns over to your child outright at 18 or 21, with no conditions whatsoever. A trust is legally distinct from a UTMA account, and it gives you something a custodial account never can: lasting control over how and when the funds are used. For larger gifts, or for any parent who wants real say over the outcome, a trust account for a child is the stronger structure.

Why New York Parents Set Up a Trust Fund for a Child

The reasons are rarely about wealth alone. Most parents who consider setting up a trust for a child are thinking about timing, protection, and peace of mind.

You may want to keep a young adult from receiving a large sum before they are ready for it. You may want to shield an inheritance if your child later faces a divorce, a lawsuit, or creditors. You might be planning for a blended family, where you want to be certain that the money reaches your own children rather than getting tangled in someone else’s estate. Some parents are simply trying to avoid the delay and public exposure of New York’s Surrogate’s Court, since assets held in a properly funded trust pass to a child without going through probate at all. You can read more about that process in the official guidance from the New York State Unified Court System.

A trust also answers a question every parent eventually asks. If something happened to you tomorrow, who would handle the money, and would they handle it the way you would want? A trust puts that answer in writing.

Picture a couple in Queens with a 12 year old and a college savings habit. Without a trust, everything they have set aside lands in their child’s lap at 18, right around the time most teenagers make their least careful decisions. With a trust, they can release a portion for tuition, hold the rest until 30, and name an aunt as trustee to keep things steady if they are no longer around. Same money, completely different outcome. That is the practical difference a trust makes for an ordinary New York family, not just for the wealthy.

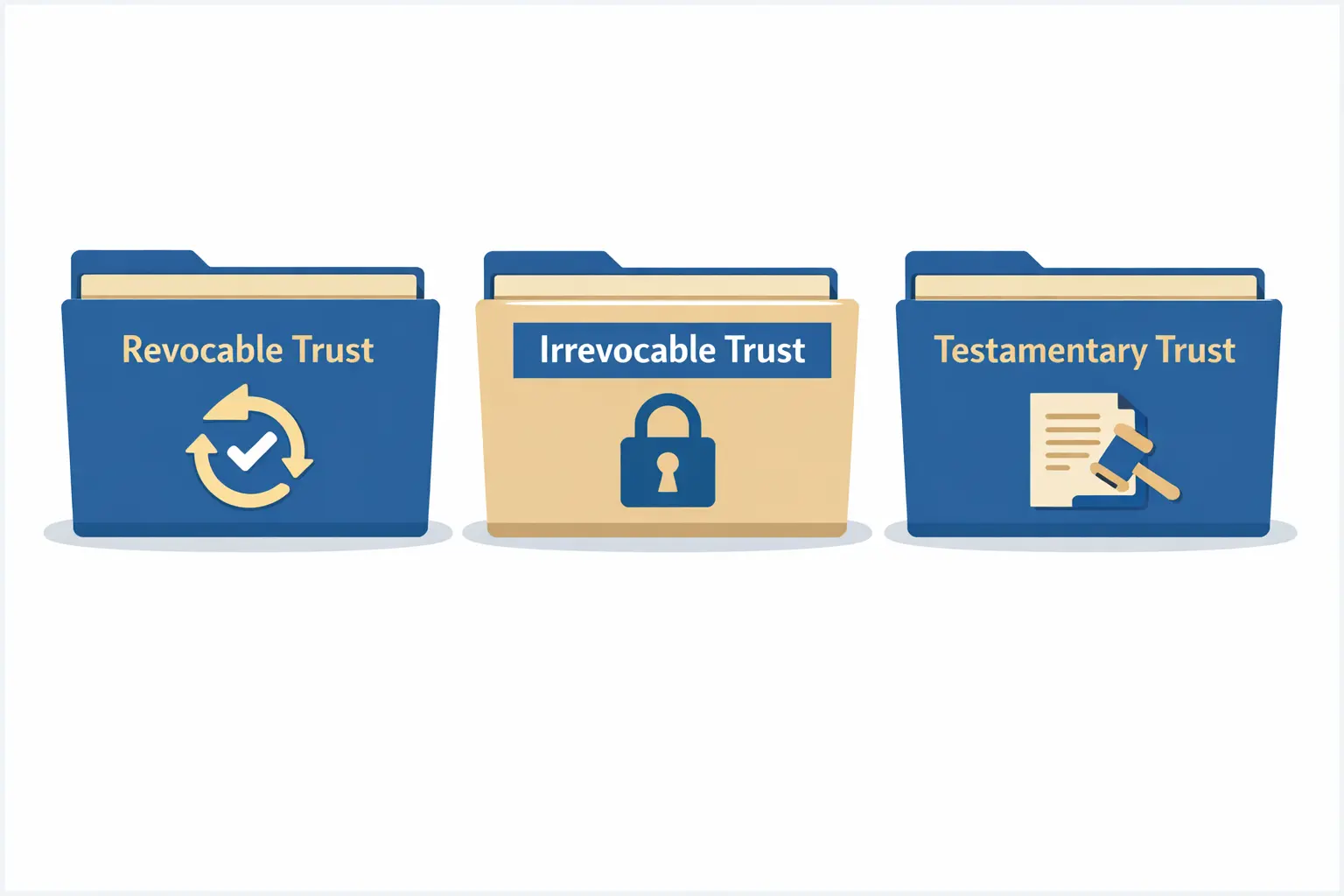

The Types of Trust You Can Use

There is no single “child’s trust.” Instead, you choose the structure that fits your goals. Three options cover the vast majority of New York families.

Revocable living trust

A revocable trust is one you create during your lifetime and can change or cancel whenever you like. It offers flexibility and keeps the assets under your influence while you are alive, then passes them to your child outside of probate when you pass away. If this is the route you are leaning toward, our guide on how to set up a living trust in New York covers the mechanics in depth.

Irrevocable trust

An irrevocable trust is far harder to alter once it is signed, and that is precisely its strength. Because you give up direct control of the assets, they generally sit outside your taxable estate and enjoy stronger protection from future claims against you or your child. Parents who want the firmest possible shield around an inheritance often choose this structure, despite the loss of flexibility.

Testamentary trust

A testamentary trust is created through your will and only springs into existence after you die. It costs little to put in place now, since it lives inside a document you should have anyway, and it is a common choice for parents who want a trust to activate only if they are no longer here. You can see how this works in our overview of a testamentary trust created through your will.

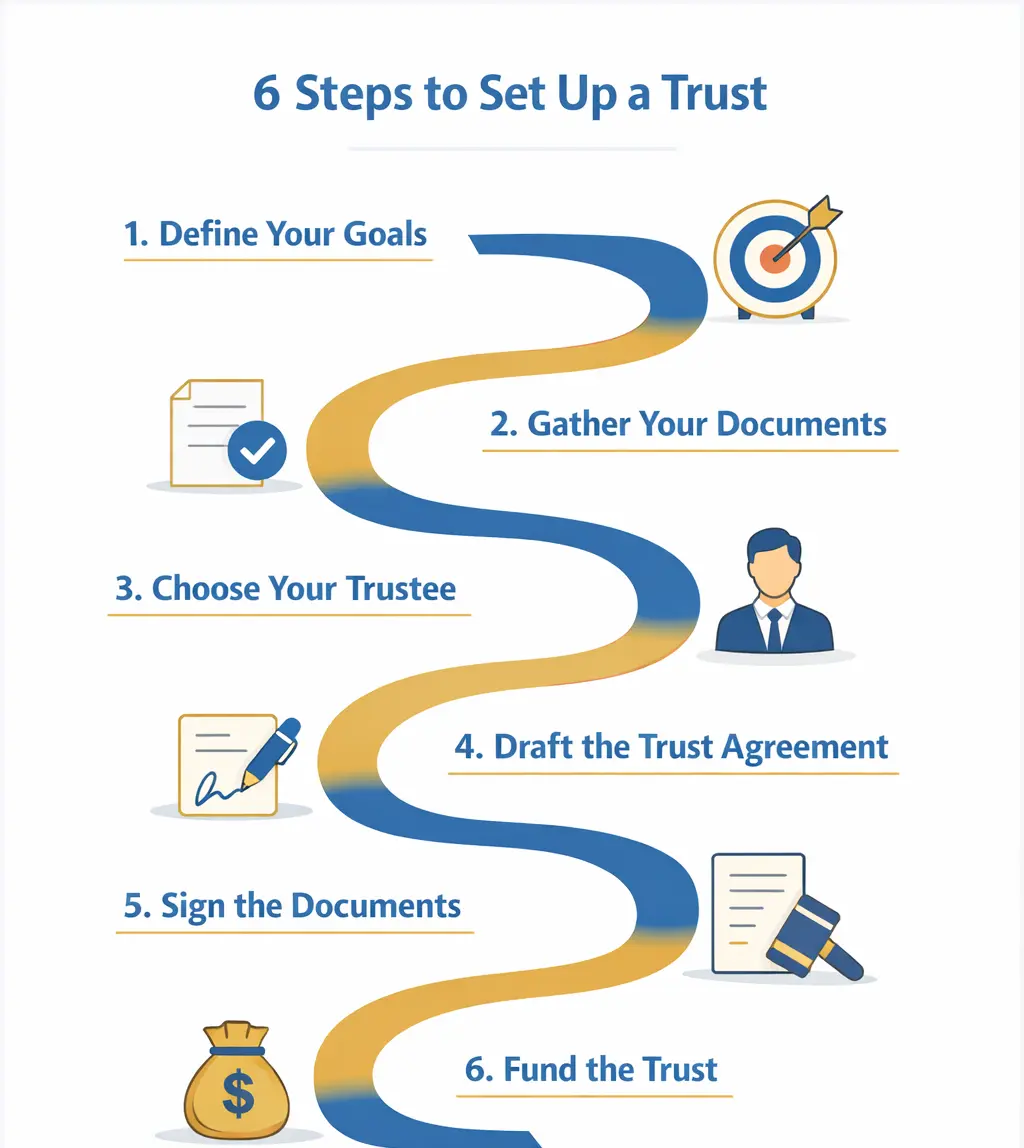

How to Set Up a Trust Fund for a Child in New York, Step by Step

Here is the path from idea to a working, funded trust. None of these steps is complicated on its own, but each one matters, and skipping any of them is where most homemade trusts fall apart. Parents often ask how to open a trust fund for a child as though it were a single form to sign. It is closer to building something: a short series of decisions, each one shaping the next.

Step 1: Decide what you want the trust to do

Start with the outcome, not the paperwork. Are you protecting a large inheritance, or simply guiding a smaller gift toward college? Do you want money released at certain ages, or only for defined purposes? Write down your intentions in plain language first. Everything else flows from this.

Step 2: Choose the type of trust

Match your goals to the revocable, irrevocable, or testamentary structure described above. Many families end up using a revocable living trust for control during life, or a testamentary trust folded into a will. The right answer depends on your assets, your family, and your comfort with giving up flexibility.

Step 3: Choose your trustee

The trustee will manage and protect the money, so this is one of the most important decisions you will make. It can be a trusted family member, a close friend, a professional, or a bank’s trust department. We cover what to look for in the section below, because choosing the wrong person is a costly error.

Step 4: Name the beneficiary and write the terms

Name your child clearly, then spell out the rules. State the ages or milestones for distributions, the purposes the funds may serve, and what happens if your child passes away before the money is fully paid out. This is the heart of the trust, and vague wording here causes real problems later.

Step 5: Sign the trust the way New York law requires

A trust is only valid if it is executed correctly. Under New York’s trust law, a lifetime trust must be in writing and signed and acknowledged by you, and by a trustee if you are not serving alone, in front of a notary in the same manner as a deed, or alternatively signed before two witnesses. A trust scribbled and stuffed in a drawer without these formalities may be worth nothing when your family needs it most.

Step 6: Fund the trust

This is the step people forget, and it is the single most common reason trusts fail. A trust controls only the assets you actually move into it. You have to retitle accounts, change beneficiary designations, or transfer property into the trust’s name. When you add cash gifts each year, keep an eye on the annual gift tax exclusion, which the IRS sets at $19,000 per recipient for 2026. Staying at or below that figure means no gift tax return and no dent in your lifetime exemption, as confirmed by the IRS gift tax rules.

Choosing the Right Trustee

Think of the trustee as the person who steps into your shoes for the money. They will follow your instructions, but they will also use judgment when life throws something your trust did not predict.

Look for someone honest, organized, and financially level headed, with the time and willingness to take the role seriously. Consider how they get along with your child, since this relationship can last for years. A relative keeps it personal and inexpensive but may struggle with conflict or paperwork. A professional or a bank’s trust department brings experience and neutrality at a cost. Many parents name joint trustees to balance the two, pairing a family member with a professional.

One more point that surprises people. New York gives a child certain rights as a beneficiary, including the right to be kept reasonably informed. A good trustee respects that, which is one more reason to choose carefully.

Always name a backup as well. People move, fall ill, or simply step down, and a trust without a named successor can stall exactly when your child needs it. If you are setting aside money for more than one child, a single trust fund for children with clear shares, or a separate trust for each, both work. The right choice depends on whether you want the money pooled or kept strictly equal, and a short conversation with an attorney usually settles it quickly.

How Much It Costs to Set Up a Trust in New York

Cost is usually the first question, so let me be straight about it. The honest answer is that it depends on the complexity of your situation, but the question of how much it costs to set up a trust in New York has a useful range.

A straightforward trust drafted by an attorney generally falls within a few thousand dollars, and a trust built into a fuller estate plan with a will and powers of attorney often costs more because you are getting more. Online templates advertise far lower prices, and for a reason. They cannot ask about your family, they will not catch the New York signing rules in Step 5, and they leave the funding entirely up to you. When a template fails, the cost is paid by your child, in court, at the worst possible time.

Spending sensibly now is almost always cheaper than fixing a broken trust later. It also helps to think of the price as covering two different things. Part of it is the document itself. The larger part is the judgment that goes into it: the questions a good attorney asks, the New York specific rules they apply, and the funding guidance that keeps the trust from sitting empty. A cheap document with no advice is the expensive option in disguise.

Common Mistakes Parents Make

The first and biggest is never funding the trust, which leaves a perfectly drafted document controlling nothing. The second is vague terms, where “for my child’s benefit” gives the trustee no real guidance and invites disputes. The third is naming the wrong trustee, often a relative chosen out of loyalty rather than ability. The fourth is relying on a generic template that ignores New York law. The fifth is creating the trust and then never updating it as your family, your assets, and the tax rules change.

Two related steps often get overlooked entirely. If you have minor children, make sure your plan also lets you name a guardian for your children, since a trust handles money but not who raises your child. And if your child has a disability, a standard trust can accidentally disqualify them from public benefits, which is why a child with special needs usually needs a specially drafted trust instead.

If you want to understand the broader picture before you decide, our explainer on what a family trust is and our pillar on how to set up a trust in New York sit alongside this guide, and grandparents will find our piece on a trust fund for grandchildren helpful. Whatever structure you choose, take the time to learn what assets to put in a trust so the funding step never gets missed.

Set Up Your Child’s Trust the Right Way

A trust fund is one of the most caring things you can build for a child. Done well, it protects them when they are young, guides them as they grow, and quietly does its job whether or not you are there to watch. Done poorly, it becomes a piece of paper that promises everything and delivers nothing.

At Bartal Law, we help New York parents create trusts that actually work, drafted to the letter of New York law, funded correctly, and built around your family rather than a template. If you are ready to turn your intentions into a plan your child can count on, we are ready to help. Mention this blog and we’ll waive the $350 session fee.